Are you tired of wondering where your money goes every month? You’re not alone. Many people struggle with managing their finances not because they don’t earn enough, but because they lack a clear budgeting plan.

In this guide, you’ll discover how to embrace budgeting as a powerful tool to regain control of your finances, reduce stress, and achieve your financial goals.

How to Take Control of Your Finances with Smart Budgeting

Most times we run into confusion and are unable to take control of most situations because of our inability to plan and budget ahead. Budgeting is not the enemy here, it should be embraced, it lets you know that you got most things under control and knowing that no matter how huge the task is you can always plan, and budget ahead leaves your mind not shattered but calm.

That feeling of having your necessary bills all covered even before the finance comes in, that feeling of giving your money a direction and purpose, being able to control and trace how it’s been spent, knowing that your hard-earned salary is not spent recklessly, is an underrated golden feeling. And after a long-term plan, the satisfaction you get pulling through to the end and knowing that you nailed it is out of this world, it gives in-depth joy, and a strong motivation to even set higher goals and achieve them.

If you’re tired of treating budgeting like it’s some kind of scary monster under the bed, it might be time to try a different approach. Here’s a simple game-plan to get a handle on your money without losing your sanity.

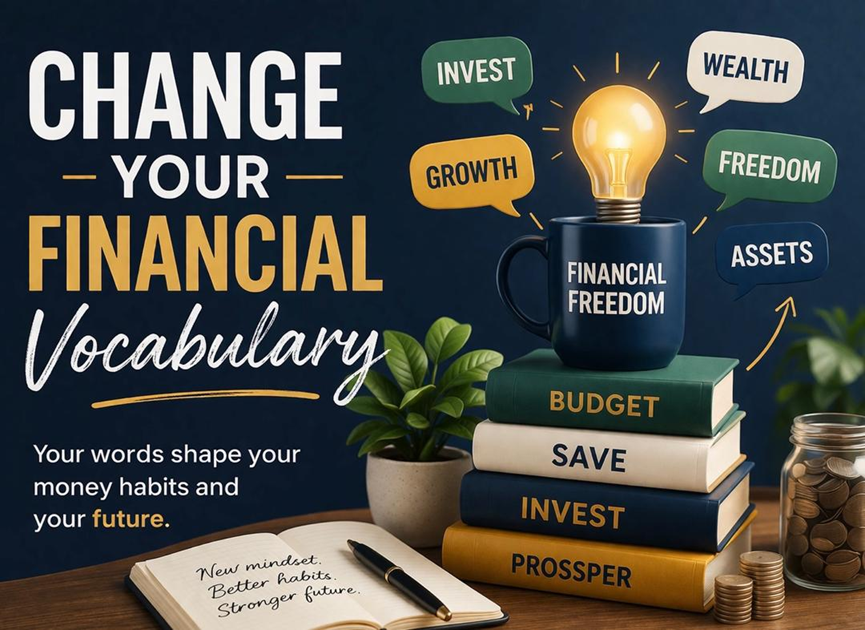

A. Change Your Financial Vocabulary

Words have immense power over our subconscious minds. You must permanently remove the phrase "I can't afford it" from your vocabulary. Saying "I can't afford it" makes you a victim of your circumstances. It implies you are powerless.

Instead, start saying, "That doesn't align with my financial goals right now," or "I choose to allocate my funds elsewhere."

If your friends ask you to go to an expensive concert, and you are saving for a house, don't say "I can't afford it." Say, "I'm choosing to put my money toward my house fund this month, but let's grab a coffee instead!" This subtle shift in language transforms you from a helpless victim into an empowered architect of your own life.

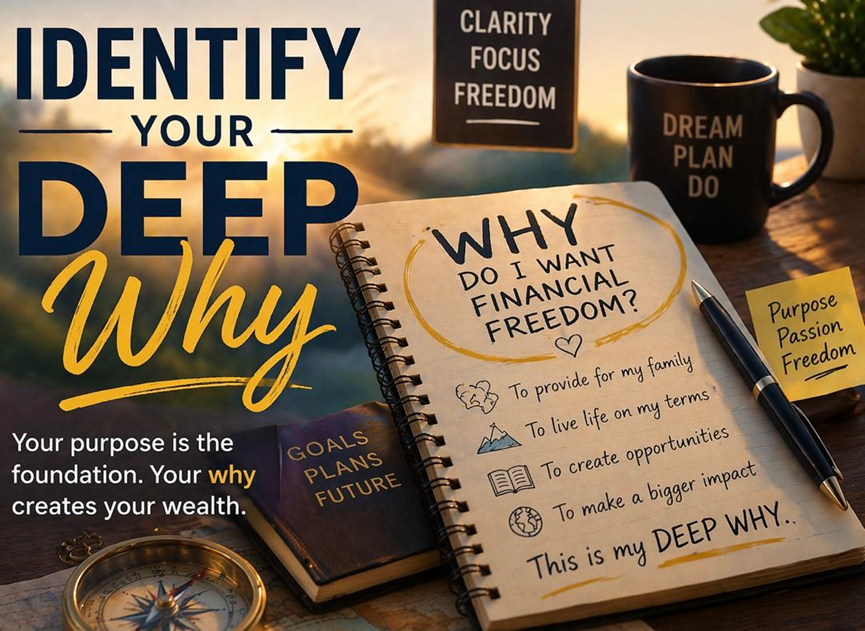

B. Identify Your Deep "Why"

Author Simon Sinek famously said, "Start with Why." If your only reason for budgeting is "because I'm supposed to," you will quit the moment things get hard. You need a visceral, emotional reason to stick to your plan.

Dig past the surface-level goals.

• Surface Goal: "I want to save #1,000,000."

• Deep Why: "I want to save #1,000,000 so I have a six-month emergency fund, which means I will finally have the courage to quit my toxic job and start my own business without fearing I'll end up homeless."

Keep this "Why" front and centre. Write it on a sticky note and put it on your bathroom mirror. Wrap it around your credit card. When you are tempted to impulse-buy something you don't need, your "Why" will give you the strength to walk away.

C. Automate Your Financial Life (Build a Robot Assistant)

Willpower is for amateurs; systems are for professionals. You should not be relying on your memory or your discipline to transfer money to your savings account every month.

Set up an "Automation Engine." Have your HR department split your direct deposit so that 15% goes directly into a high-yield savings account or investment account, and 85% goes to your checking account. Set all your fixed bills (utilities, insurance, internet) to autopay on a credit card, and set that credit card to auto-pay the full statement balance from your checking account every month.

When you automate your finances, you only have to be disciplined once during the setup phase. After that, the system builds your wealth in the background while you sleep.

D. Budgeting as a Team (Ending the Money Fights)

If you share finances with a partner, budgeting is often a battleground. Usually, one person is the "Saver" (who views money as security and safety), and the other is the "Spender" (who views money as a tool for experiences and freedom).

When the Saver tries to restrict the Spender, the Spender feels suffocated. When the Spender buys things, the Saver feels terrified.

To stop the fights, you must stop using the budget as a weapon to police each other. Instead, sit down with a glass of wine and dream together. Agree on your shared "Hell Yes" goals (a house, a vacation, retiring early).

Then, implement the ultimate relationship hack I call the “Individual Guilt-Free Spending Allowances”. Both partners get an agreed-upon amount of money each month (e.g., #30.000) transferred to their own separate accounts. The Spender can use their #30,000 to buy expensive shoes, and the Saver cannot say a word. The Saver can take their #30,000 and hoard it in a savings account, and the Spender cannot say a word. It preserves individual autonomy while guaranteeing the team's goals are met.

E. Practice Radical Financial Self-Compassion

You are going to mess up. You are going to have a month where you blow past your dining-out budget, or you forget to cancel a free trial and get charged #10,000.

When this happens, you must practice radical self-compassion. Do not beat yourself up. Do not enter the shame spiral. Do not abandon the system. Acknowledge the mistake, figure out what triggered the impulse (Were you stressed? Tired? Hungry?), adjust your budget for the following month to absorb the hit, and move forward. In the grand scheme of a 40-year wealth-building journey, a #10,000 mistake in a single month is a rounding error.

There is no perfection at first, consistency is what keeps it going, consistency beats perfection every single time.

The Four Budgeting Frameworks

Here are four popular frameworks. I’ve discussed these briefly in an earlier post, but it’s worth taking a closer look at each of them.

1. The 50/30/20 Rule (The "Big Picture" Budget)

This is the ultimate budget for people who hate budgeting. Popularized by Senator Elizabeth Warren, this method requires almost zero daily tracking. You simply divide your after-tax income into three broad buckets:

• 50% for Needs: Rent, groceries, utilities, minimum debt payments, health insurance. (The things you must pay to survive).

• 30% for Wants: Dining out, hobbies, vacations, Netflix, shopping. (The fun stuff).

• 20% for Savings & Investing: Contribution, emergency fund, extra debt payoff. (Paying your future self). As long as your automated transfers hit these percentages, you don't have to track individual purchases.

2. Zero-Based Budgeting (The "Every Naira Has a Job" Method)

This is for people who want total control and maximum efficiency. The rule is simple: Income minus Expenses must equal exactly zero. If you make #400,000 a month, you must assign exactly #400,000 to specific categories before the month begins. You allocate money for rent, food, investments, and fun, until there is #0 left unassigned. Apps like YNAB (You Need a Budget) or EveryDollar are built entirely around this highly effective philosophy.

3. The Envelope System (The "Tactile" Budget)

If you struggle with credit card debt and the frictionless nature of Apple Pay, this old-school method is a lifesaver. You take your "Wants" and "Variable" categories (like Groceries, Dining Out, and Entertainment) and you pull that exact amount out of the bank in physical cash. You put the cash in labeled envelopes. When you go to a restaurant, you pay from the "Dining Out" envelope. When the envelope is empty, you stop eating out for the month. The psychological pain of handing over physical cash is proven to reduce impulse spending.

4. Reverse Budgeting (The "Pay Yourself First" Method)

This is the ultimate lazy person's guide to wealth. Instead of tracking your expenses to see what you can save, you automate your savings first, and live off whatever is left. On payday, your bank automatically transfers 20% of your income to your investments and savings accounts. Once that money is safely tucked away, you are free to spend the remaining 80% in your checking account however you please, without tracking a single category.

The initial setup of any of these systems might take an hour or two on a Sunday afternoon. But once the automation is in place, ongoing maintenance can take as little as 10 to 15 minutes a week.

As an individual, you have the best understanding of your spending habits and your budgeting weakness and know what would work best for you among these frameworks. They all have a common purpose to walk you through budgeting. Do not go a framework too harsh or too cool, remember in every budgeting, there should be room for emergencies, and you can always have a little bit of fun, like the world would say; live a little too while you spend wisely.

Budgeting is not punishment; your budget is your blueprint for freedom. The biggest misconception about budgeting isn't just a harmless misunderstanding; it is a psychological barrier that keeps millions of people trapped in a cycle of financial anxiety, preventing them from realizing their full potential.

By viewing budgeting as a tool for restriction, we deny ourselves the very thing it promises to deliver, absolute freedom. Freedom from the suffocating weight of consumer debt. Freedom from the 3:00 AM panic attacks about how rent will get paid. Freedom to pursue your passions, to take risks, to care for your loved ones, and to live the life you genuinely desire, rather than the one dictated by impulse, targeted advertising, and external societal pressures.

Money has no intrinsic value. It is just paper and digital pixels. Its only true value is that it represents stored energy and stored time. When you master your budget, you unlock the ability to convert that stored energy into a life you actually love.

So, it is time to banish the budgeting bogeyman once and for all.

Pick up your pen, download that app, or open that spreadsheet. Design your budget not as a list of limitations, but as a master blueprint for the extraordinary life you are ready to build. You hold the power to direct every single dollar, to align your capital with your deepest values, and to construct a future filled with genuine abundance.

It is not about how little you can spend. It is about how intentionally you can live.

The cage is open. The permission slip is signed. It’s time to take your life back.

In a world filled with endless inspiration, having too many ideas can be just as paralyzing as having none. This article explores how to filter through the noise, identify profitable opportunities, and transform creativity into success.

Planning a trip with friends but worried about your finances? Discover practical budget travel tips, smart saving strategies, and stress-free ways to enjoy group adventures without going into debt. Travel smarter without sacrificing fun.

Learn how to save for your dream vacation without falling into credit card debt. Discover practical budgeting tips, smart saving strategies, and proven financial hacks for stress-free, debt-free travel.