Discover the 5 fundamental money rules schools never taught you. Learn how to build wealth, escape financial stress, and take control of your financial future. These rules can completely change how you think about wealth and financial security.

5 Fundamental Money Rules Schools Never Taught Us (But Everyone Should Know)

If you’ve ever felt like you’re working harder every year but somehow not getting much further ahead financially, you’re not alone. Many people feel this exact frustration. They work long hours, follow the advice they were given growing up, try to save when they can, and yet financial security still feels just out of reach.

The reason for this is simpler than most people think.

Most of us were never actually taught how money works.

School taught us how to pass exams, how to follow schedules, and how to become productive workers. Those things are useful, but they don’t necessarily teach us how to build wealth. In fact, the traditional education system was originally designed during the industrial age to prepare people for stable employment in factories, offices, and institutions.

That system assumed something very different about the world than what we live in today. It assumed that if you worked hard for a company, stayed loyal, saved money carefully, and avoided major mistakes, you would gradually become financially secure.

But the modern economy works differently.

If you look closely at people who achieve real financial independence, you’ll notice something interesting: they don’t just work harder than everyone else. Instead, they tend to follow a completely different set of financial principles. These principles are not secret formulas or complicated tricks. In fact, they are surprisingly simple once you understand them. The problem is that most people never hear about them early enough.

Let’s walk through five of the most important rules.

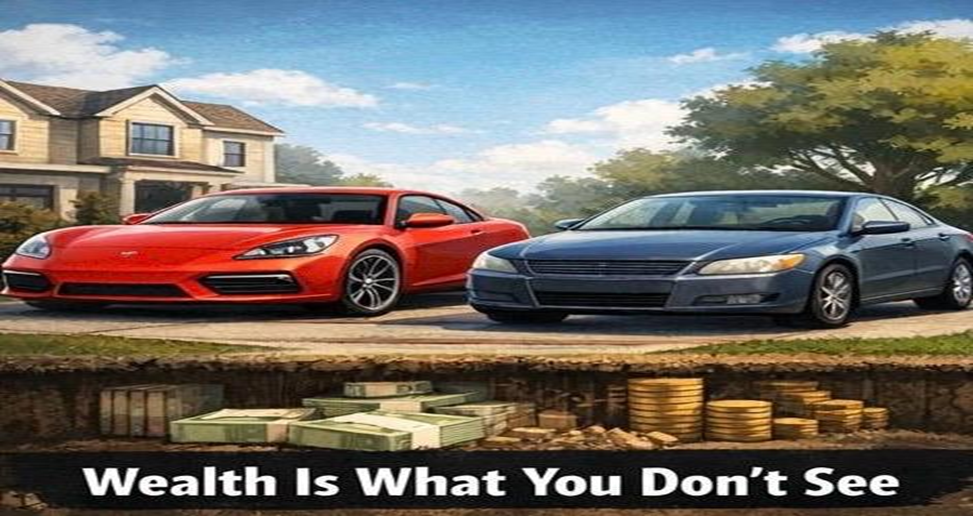

Rule #1: Wealth Is What You Don’t See (The Porsche Illusion)

One of the biggest misconceptions about money is how we measure success.

Most people naturally assume that someone who looks wealthy must be wealthy. Expensive cars, luxury watches, designer clothing, and big houses create the impression that someone is financially successful. It is human nature to judge financial success by what we can see because we cannot look at someone's bank account or read their credit card statements, we rely on visual proxies to gauge how successful they are.

But as Morgan Housel brilliantly points out in his book The Psychology of Money, this relies on a massive optical illusion. We are constantly confusing being "rich" with being "wealthy."

Imagine sitting at a traffic light and seeing someone pull up beside you in a brand-new sports car. Instinctively, many people think, “That person must be doing really well.” But appearances can be extremely misleading.

There is a very important difference between being rich and being wealthy, and the two are often confused. Being rich usually means someone has a high income or spends a lot of money. It’s about visible consumption. A rich person might have a large salary and an impressive lifestyle that everyone around them can see.

But wealth is something very different. Wealth is the money that has not been spent. It’s the savings, investments, and financial reserves that exist quietly in the background. Unlike luxury cars or expensive clothes, wealth is usually invisible. You cannot easily see it when you look at someone.

This is a difficult concept to internalize because it goes against everything society markets to us. We are sold the idea that the whole point of making money is to spend it, so people know you have money. But the paradox of wealth is that spending money to show people how much money you have is the fastest way to have less money.

This is why judging financial success by appearances is so unreliable.

Someone driving an $80,000 car might be heavily in debt. Their lifestyle could depend entirely on their next paycheck. If their income suddenly stops, the expensive lifestyle disappears quickly.

On the other hand, someone driving an older, modest car might quietly have hundreds of thousands of dollars invested in stocks, businesses, or real estate. The second person might look ordinary but financially they are far more secure. This idea becomes even more important when we consider something called lifestyle creep.

Lifestyle creep happens when a person increases their spending every time their income rises. When someone receives a raise, they often celebrate by upgrading their lifestyle. Maybe they move into a better apartment, lease a nicer car, or begin spending more on entertainment and dining.

At first this feels like progress. But if spending rises at the same pace as income, then actual wealth never grows. Many people earn more money over time but remain stuck in the same financial position because their expenses grow just as quickly as their earnings.

Real wealth works differently.

Instead of spending every increase in income, wealthy individuals often allow their savings and investments to grow quietly in the background. Over time, these hidden resources become powerful. The true purpose of money is not to impress other people. The real power of money is the freedom it provides.

Wealth gives you options. It gives you the ability to leave a job that is making you miserable. It gives you the freedom to take time off if a family member needs you. It allows you to pursue opportunities without constantly worrying about survival. In other words, wealth buys something much more valuable than status. It buys control over your time and your life.

And that is why the first rule of money is so important:

If you want to become wealthy, you must stop focusing on looking rich and start focusing on building what people cannot see.

Rule #2: You Can’t Sell Your Time Forever

You are taught a very simple formula about money growing up. If you want to earn more, you work more. You work harder, longer and your way up the ladder.

At first, that advice makes sense. In fact, early in your career it’s usually the best thing you can do. Developing skills, becoming good at your job, and earning a higher salary can dramatically improve your life. But there’s a hidden problem with this system that people usually discover much later. Your income is tied directly to your time and time is limited.

No matter how talented you are, no matter how valuable your work becomes, there are still only 24 hours in a day. You can increase your hourly rate, but you can’t multiply your hours forever. This is why so many highly paid professionals still feel financially stuck. From the outside, they appear very successful. They earn great salaries, live in nice homes, and drive expensive cars. But their lifestyle depends on one thing: continuing to work.

If they stop working for a few months, their income slows down or stops completely. That pressure never really disappears. This is the trap of trading time for money.

It’s not necessarily a bad system. It's how most people begin building their financial lives. The problem is when it becomes the only system you rely on. At some point, if you want real financial freedom, something must change. Instead of only selling your time, you must start owning things.

Ownership changes how money flows into your life.

When you own something whether it’s a small business, investments, intellectual property, or a digital product, you create something that can continue producing value even when you’re not actively working at that moment.

Think about something simple like a book. An author might spend months writing it. But once the book exists, people can continue buying it for years. The author doesn’t need to rewrite the book every time someone purchases a copy.

The same thing happens with many things in the modern economy. A piece of software, an online course, a useful template or too, a small business or even a YouTube video or article. All these things take effort to create, but once they exist, they can continue generating value without repeating the same work every single time.

As the entrepreneur and philosopher Naval Ravikant famously stated: "You will never achieve true financial freedom by renting out your time."

When you rent out your time, you are trading a strictly finite resource (the hours of your life) for money. To break this cycle, you have to completely sever the link between your inputs and your outputs. You have to acquire equity.

Equity simply means owning a piece of a system that works while you sleep. When you own equity, you step into the world of leverage. Leverage is the magical force that allows you to put in one hour of work and get the results of one hundred hours. This simply means that your effort reaches far beyond the hours you personally worked. Instead of your income being limited to the time you put in today, the value you created continues to work for you later.

In the modern economy, there are three main ways to build this leverage:

Labor Leverage (Other people working for you): This is the oldest form of leverage. You start a business and hire employees. While you are sleeping, your team is operating the store, writing the code, or making the sales. It is highly effective, but it is also messy. Managing human beings requires immense leadership, patience, and capital.

Capital Leverage (Your money working for you): This is the leverage of the investor class. Think of every dollar you save and invest as a tiny, tireless employee. That dollar never sleeps, never takes a sick day, and works 24/7 to earn you more pennies. When you buy index funds, you are buying tiny fractions of equity in thousands of profitable companies. The CEOs of those companies are now waking up every morning and working for you.

Permissionless Leverage (Code and Media): This is the great equalizer of our time, and it is entirely new to human history. You can write a book, record a podcast, design a digital template, or build a piece of software. You create it once perhaps at 2:00 AM on a Tuesday from your kitchen table and it can be sold, downloaded, or consumed a million times with zero extra effort on your part. You don't need anyone's permission to create it, and the cost of replicating it is zero.

This doesn’t mean everyone should quit their job tomorrow and start a company. That’s not realistic for most people. But it does mean that over time, your goal should slowly shift. At the beginning of your career, your focus is mostly on earning. Later, the focus should gradually shift toward owning. Owning investments, assets, and things that can grow without requiring your constant attention.

Start asking yourself: Am I only getting paid for the hours I work, or am I building something that will pay me when I stop?

When that starts happening even in small ways, your financial life begins to change. The moment you own something that earns money without needing your time every single day, you’ve started building a system that works with you instead of only depending on you.

Your ultimate career goal shouldn't just be to negotiate a higher hourly rate. It should be to slowly, methodically transition from a wage-earner to an equity-owner.

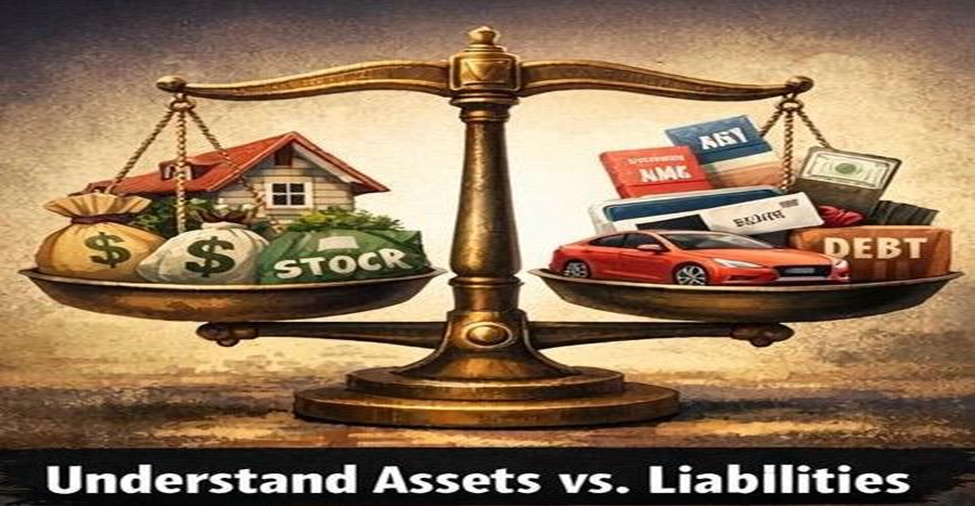

Rule #3: The Middle-Class Trap (redefining assets and liabilities)

You ask a traditional accountant to list your assets, they will point to your driveway and your living room. They will tell you that your house, your car, and maybe even your designer watch are your greatest financial assets because they have "resale value."

But if you ask a wealthy investor, they will tell you that exact mindset is the primary reason the middle class stays broke.

You can do everything “right” financially, get a decent job, earn a steady paycheck, maybe even get a raise every few years and still feel like you’re not really getting ahead. The strange part is that a lot of people who work incredibly hard still end up stuck in the same financial position for decades.

In his foundational book Rich Dad Poor Dad, Robert Kiyosaki stripped away all the complex, corporate accounting jargon and redefined these two words based on one simple, undeniable metric: cash flow.

Here is the only definition that actually matters in the real world:

An Asset puts money into your pocket, whether you work or not.

Liability takes money out of your pocket.

It sounds almost too simple, but applying this lens to your life is a brutal awakening. If someone is earning more money than they used to, shouldn’t their financial situation naturally improve? In theory, yes. But in reality, something else usually happens. Most people increase their spending at the same pace as their income.

The cycle of the middle class says you earn a paycheck. You immediately use that paycheck to buy liabilities that look like assets (a nicer car, a bigger house, a boat, expensive subscriptions). Because these liabilities constantly drain your cash, you have to work harder and longer to maintain them. You get a raise, and you immediately buy a more expensive liability. You are trapped on a treadmill, running at full speed just to stay in the exact same place.

The cycle of the wealthy on the other hand says, you earn a paycheck. You live below your means, and you use your extra cash to buy actual assets. You buy dividend-paying stocks. You buy a cash-flowing rental property. You invest in a profitable online business. You buy bonds. You build a portfolio of little machines that print money for you 24 hours a day.

Here is the ultimate secret of the wealthy: They do not buy luxuries with their own labor.

The wealthy don't buy the Porsche with their salary. They buy an asset, and they let the cash flow from the asset buy the Porsche. If the asset stops paying, they don't buy the car. Their foundational wealth is never touched; it is only used to acquire more assets.

A raise comes in, and naturally life gets upgraded a little. Maybe it’s a nicer apartment or it’s a newer car. Maybe it’s eating out more often, taking better vacations, or buying things that once felt out of reach. None of those things are bad by themselves. The problem is that the upgrades rarely stop. Over time, the entire paycheck gets absorbed into maintaining the new lifestyle. And this is where the trap starts forming.

You appear financially successful and still feel constantly pressured by money. This lifestyle has grown so large that it requires a steady stream of income just to keep everything running. Wealthy investors tend to approach this differently. Before upgrading their lifestyle, they focus on buying things that produce income instead of consuming it. Things like businesses, investments, or assets that generate cash flow. The idea is simple when you think about it. Instead of your paycheck paying for everything, you slowly build things that start paying you back. When this happens, your lifestyle is no longer supported entirely by your job. Some of it is supported by the things you own. And that’s usually the point where people realize they’ve finally stepped outside the trap.

Take a hard look at your bank statement this month. Audit your life. Are you spending your hard-earned time collecting assets that will eventually set you free? Or are you just collecting expensive liabilities that are keeping you trapped?

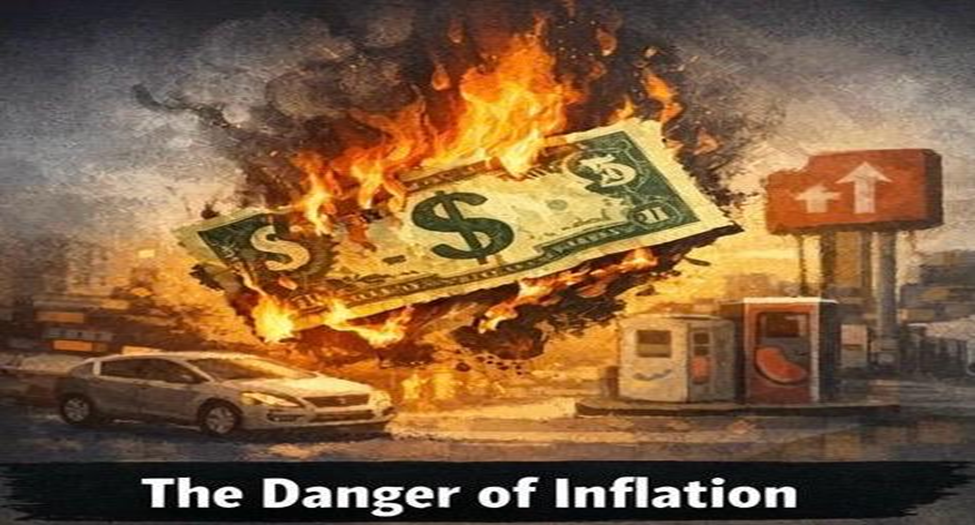

Rule #4: Cash Slowly Loses the Game

Ever since we were kids dropping pennies into a piggy bank, we’ve been told that saving money is the ultimate responsible thing to do. We were taught that if you just stash your cash in a safe, boring bank account, you’re doing great.

And honestly, it feels incredibly safe. When you log into your banking app on January 1st and see $10,000, and then you log in on December 31st and still see $10,000, your brain does a happy little dance. The number didn't go down and so, you didn't lose anything.

But here is the brutal, hidden truth about money: you in fact did lose something. You are falling victim to an invisible tax called inflation.

Billionaire investor Ray Dalio has this famous saying: "Cash is trash." Now, he doesn't mean cash is literally useless. What he means is that cash is a terrible place to store your wealth long-term.

Think of your savings account not as a steel vault, but as a melting ice cube sitting on your kitchen counter.

Let’s break down the math in a way that makes sense. When the government prints trillions of dollars to stimulate the economy, there is suddenly way more money floating around out there. But there isn't magically more stuff to buy. More dollars chasing the same amount of groceries, houses, and cars means the price of all those things goes up. So, if inflation is running at, say, 4% a year, and your bank is paying you a measly 0.5% in interest, you are quietly losing 3.5% of your purchasing power every single year.

The money isn't physically disappearing from your account. The $10,000 is still there. But what that $10,000 can actually buy is shrinking.

Think about it: ten years ago, $100 bought you a massive cart overflowing with groceries. Today? That same $100 barely covers two bags of basics and a pack of chicken. That is the melting ice cube in action.

Now, don't get me wrong. You absolutely need some cash. You need an emergency fund of 3 to 6 months of living expenses sitting in a High-Yield Savings Account. Cash is your financial shock absorber. When your car breaks down or your roof leaks, cash keeps it from becoming a full-blown crisis.

But anything beyond that emergency fund? You have to rescue it from the melting ice cube.

To protect your wealth, you have to convert your extra cash into "hard assets". Things like stocks, real estate, or a business. You may ask why? Because when the cost of living goes up, the value of those assets usually goes up right along with it. That’s just common sense. But keeping large amounts of money sitting in cash for years is a different story. Because while that money is sitting there, the world keeps moving.

This is why some investors think about cash very differently than most people do. To them, cash isn’t really a long-term strategy. It’s more like a temporary parking spot. We tend to think risk only comes from investing or starting something new. But sometimes there’s risk in doing nothing too.

Over very long periods of time, money tends to grow when it’s connected to things that are producing value like businesses, innovation, real estate, markets, and the broader economy.

Rule #5: The Magic of Asymmetric Bets (Or, How to Fail Your Way to Success)

Let's talk about risk. If you're anything like me, you were probably raised to be terrified of it. We're taught to play it safe, get a stable job, keep your head down, and don't rock the boat.

Because of this, most of us live highly "symmetric" lives. We make fair trades. I work for one hour; I get paid for one hour. Or I risk $1,000 in the stock market hoping to make $1,000. The downside and the upside are basically a tie.

But people who build real wealth? They don't play fair. They actively hunt for what author Nassim Nicholas Taleb calls asymmetric bets.

An asymmetric bet is just a fancy finance term for a very simple question: What is a situation where I have almost nothing to lose, but I could win massively?

Think about how this applies to everyday life. For instance, you spend $200, and a month of evenings learning how to analyze data or write good copy. The downside is capped at $200. The upside is a $20,000 bump in your salary because you just made yourself incredibly valuable.

What about this; You spend a few weekends building a digital product, maybe a budget template, a meal-prep guide, or a short e-book. The downside comes with you missing out on a few hours of watching Netflix. The upside? You put it online and it sells thousands of copies while you're sleeping.

You can try ten different things. Nine of them can completely flop. You might feel a little embarrassed, and your friends might wonder what the heck you're doing. But that one thing that works can pay off so big that it wipes out all the failures and changes your life forever.

Exceptional investors have a better understanding of this very well. They don’t expect every investment to thrive. What they look for are opportunities where the downside is limited but the upside is substantial. That imbalance is what creates the real prospect. The principles apply equally to venture capital. Out of ten startups, several will flop, a few might survive, and maybe one becomes extremely valuable. That single winner often covers the flops from the rest. This is why failure, when approached correctly, doesn’t necessarily spell trouble. If the risk is controlled and the exposure is petite, failure simply becomes part of the process.

In other words, the goal isn’t to avoid being wrong. The goal is to be wrong in ways that don’t hurt much, while leaving room for outcomes that could turn out far better than expected. That’s the quiet advantage of asymmetric bets: small, manageable losses on the downside, and the possibility of meaningful gains on the upside. And in many cases, that’s how you end up succeeding by allowing yourself enough room to fail along the way.

You literally fail your way to success.

The Bottom Line

Look, money is stressful. We all know it. But the rules of the game aren't that complicated. They’re just the exact opposite of what we were taught growing up. If you can start buying things that actually put money in your pocket and stop letting inflation quietly eat your savings, you stop running on the treadmill.

In a world filled with endless inspiration, having too many ideas can be just as paralyzing as having none. This article explores how to filter through the noise, identify profitable opportunities, and transform creativity into success.

Planning a trip with friends but worried about your finances? Discover practical budget travel tips, smart saving strategies, and stress-free ways to enjoy group adventures without going into debt. Travel smarter without sacrificing fun.

Learn how to save for your dream vacation without falling into credit card debt. Discover practical budgeting tips, smart saving strategies, and proven financial hacks for stress-free, debt-free travel.