Struggling to stick to a budget? Learn how to create a simple, realistic budget that works every month step-by-step tips for beginners and variable incomes. If you’ve ever felt like budgeting “doesn’t work,” this step-by-step breakdown will show you how to make it work for you.

How to Create a Simple Budget That Actually Works

Let me tell you a small story.

A few years ago, a friend of mine swore budgeting wasn’t for her. “Budgets are too strict,” she said. “They make me feel broke.”

Funny thing? She was always broke anyway. The problem wasn’t budgeting. The problem was her method of budgeting. Most people think a budget is a punishment. In reality, a good budget is more like a map. It shows you where your money is going and gently tells it where to stop misbehaving.

So today, let’s talk about how to create a simple budget that actually works in real life, not the kind that looks good on paper and fails by week two.

First, Let’s Redefine What a Budget Really Is;

A budget is not a list of things you can’t enjoy or a reminder that money is tight, neither a spreadsheet that stresses you out but rather, simply a plan for your money before it disappears.

If money comes in and money goes out (and trust me, it always does), then a plan is non-negotiable.

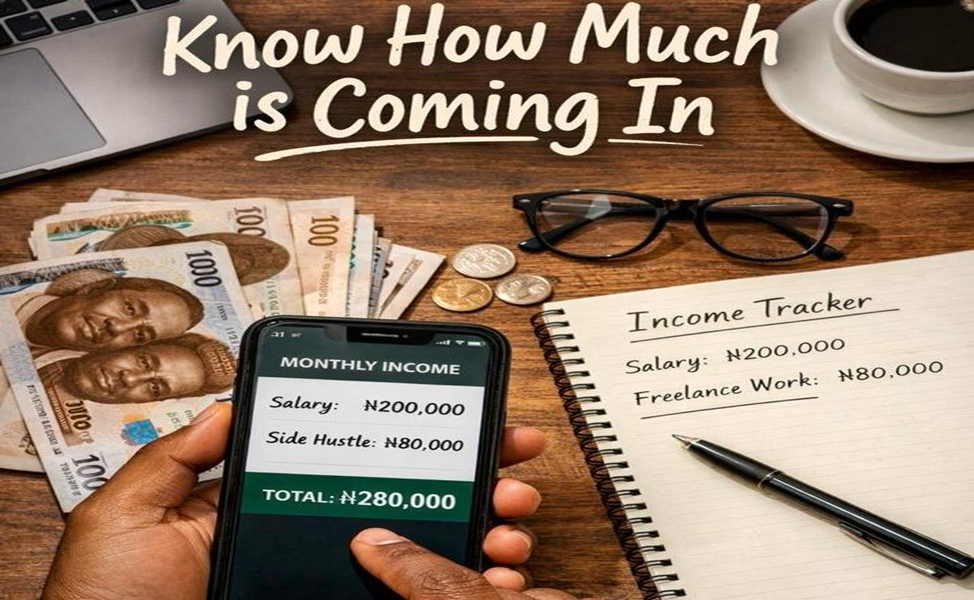

1. Know What’s Coming In (Be Honest Here)

Before you can plan your money, you need to know how much you actually have to work with. Not in your head. Not in theory. In real life.

Your income is simply the money that comes to you. This is money you can count on, touch, and spend. Income can show up in different ways, depending on your life right now. For some people, it’s a salary. For others, it’s a mix of small streams that come together. And here’s the important part. This step requires honesty.

Many people build their budget around hope instead of reality. They plan with money they haven’t received yet, and when it doesn’t come in, the budget falls apart. Then they think budgeting doesn’t work when really, the numbers were never real to begin with.

When we say “know what’s coming in,” we mean all the regular sources of money you receive, such as:

Your salary or wages

Allowance or support

Side hustle income

Business earnings

If your income changes from month to month, do not pick your best month. Use an average or the amount you’re most likelyto receive. That way, your budget works even on quiet months.

Take a moment to write down what you realistically receive in a month, not what you’re expecting, not what you’re hoping for, but what usually shows up. This number becomes the foundation of your budget. When it’s honest, everything else becomes easier to manage.

2. Track Where Your Money Is Going (This Part Changes Everything)

Imagine you earn ₦80,000 in a month. You don’t make any big purchases, so you feel like your spending is under control. But when you track your money for one week, you notice something interesting. ₦1,500 here for transport, ₦2,000 for food, ₦500 for airtime, ₦700 for a quick snack. None of it feels serious at the moment.

By the end of the week, those small amounts add up to more than ₦15,000.

That’s the power of tracking. It turns invisible spending into something you can see and understand and once you see it, you can decide what to keep, what to reduce, and what to change.

To track your money means to observe your spending as it happens.

For one week, just notice:

How much you spend on transport

What goes into food and snacks

Data and airtime expenses

Small “it’s just ₦500” purchases

Subscriptions or automatic payments you forgot about

Most people do not actually overspend in dramatic ways. It’s not always some huge, reckless decision. It’s usually small things. The little daily habits that don’t look serious on their own. Most often a snack or a motivational quote of “I deserve this” moment after a long day.

I remember a student who tracked her money for the first time. Nothing extreme. She was motivated to analyze what she spent a week doing. When she added everything up, she realized she had spent more on random snacks than she had saved. At first, she laughed about it but after a while, she went quiet. Not because she felt guilty but she then finally realized where all her spendings had gone.

That’s how change really starts. Not with pressure but with awareness. You’re not doing something wrong because you spend. You’re just seeing your habits for what they are. And there’s something powerful about that. When you can see where your money goes, it stops feeling like it disappears. You stop feeling confused and you start noticing patterns. The most important thing about this change is that you learn to adjust slowly. This quiet shift from not knowing to becoming aware is bigger than it sounds. It is the point where money stops controlling you and you begin to take control of it.

And honestly, that’s where financial freedom really begins.

3.Use the “Needs, Enjoyment, Future” Method

Once you know your income and have tracked your spending, the next step is deciding how to divide your money. This is where many people feel confused and ask “Should I save first? Spend first? Do I even have enough?”

The “Needs, Enjoyment, Future” method is a simple, logical way to make that decision. Think of it as three buckets for your money, each with its own purpose. Nothing complicated and intimidating, just a framework that works.

Needs are the essentials. The things you must pay to keep life running smoothly. Let’s say for instance; Food, rent, transport, electricity, water, internet for work.etc. These are non-negotiable. If you don’t cover your needs first, everything else falls apart. Imagine trying to save money without having money for food or transport, you would never stick to it. Needs are like the foundation of a house. If it is weak, everything else is unstable and you need to learn the habit of taking good care of that house.

Enjoyment is your permission to live a little. Life is not just about bills and responsibilities. This bucket is for the small joys like a coffee with a friend, a weekend outing, your favorite snack, or something that makes you happy. People often skip this part, thinking it’s “unnecessary,” but the truth is, a budget that doesn’t allow enjoyment rarely lasts. You will stick to it only if you feel rewarded, even in small ways.

The future is all about taking care of the you of tomorrow. This bucket includes savings, emergency funds, investments, or paying off debt. Even if you can only put a small amount aside each month, consistency matters more than size. Think of it as planting seeds. You may not see the tree today, but in time, it grows and supports you when you need it most. You learn to water that tree everyday and watch it grow.

Imagine you earn ₦100,000 a month. Using the “Needs, Enjoyment, Future” method, you might split it like this:

Needs (60%) → ₦60,000 for rent, food, transport, bills

Enjoyment (20%) → ₦20,000 for outings, snacks, treats

Future (20%) → ₦20,000 for savings or emergency fund

The beauty of this method is its simplicity. You don’t need fancy formulas. You don’t need perfect percentages. Start with rough splits that feel realistic, then adjust as you go. The goal is balance. cover what you must, enjoy life a little, and build security for the future.

You are allowed to live a life while building, but not extreme, just intentional.

4. Make It Flexible, Not Perfect

Know this and know peace, life does not follow a spreadsheet. No matter how carefully you plan your life, unexpected things happen. Your transport costs might increase, a friend invites you out last minute, or a bill shows up you forgot about. That’s normal, and it doesn’t mean your budget has failed.

A budget is a guide, not a rulebook. Its job is to give your money direction, not to trap you or make you feel guilty. Being too rigid is the fastest way to give up on budgeting entirely.

In this case, flexibility is your best friend. If one area of your budget goes over, you adjust somewhere else. Maybe you spent ₦5,000 more on transport than planned. That does not mean you cut your enjoyment completely. Maybe you reduce a small treat or postpone a non-essential purchase. Small adjustments keep your plan realistic and stress-free.

Think of it like steering a car. You don’t drive in a straight line perfectly. You adjust constantly to stay on the road. A flexible budget works the same way.

It’s also important to remember that perfection is not the goal. Your budget doesn’t have to be flawless to work. Even small, imperfect steps build good habits over time. The key is consistency. Learn to adopt a habit of checking in from time to time, making small adjustments, and staying aware of your money.

When your budget is flexible:

You feel less stressed about money.

You can handle surprises without panic.

You actually stick to your plan instead of abandoning it.

Flexibility is what turns budgeting from a chore into a helpful tool.

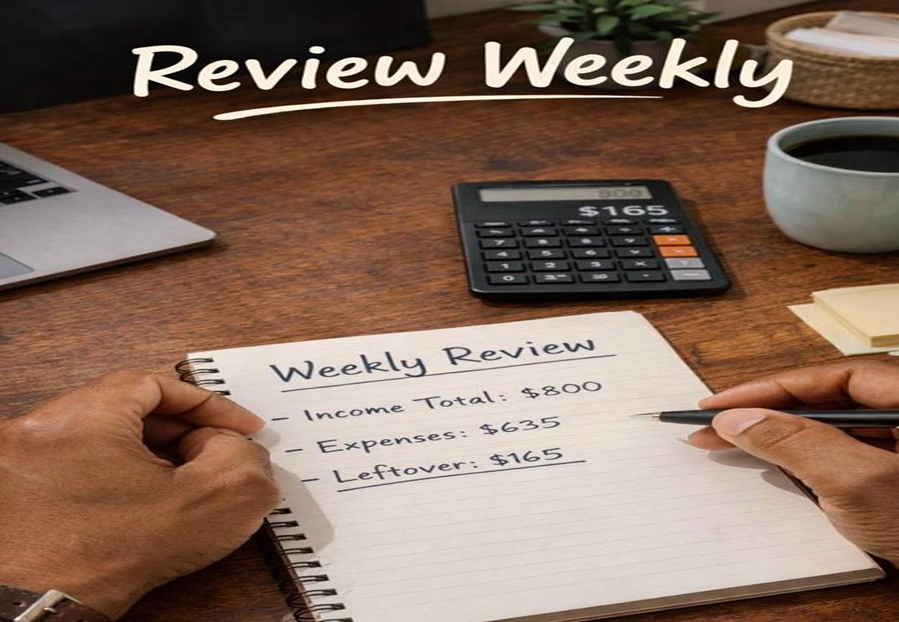

5. Review Weekly (5 Minutes Is Enough)

Think of reviewing your budget like reviewing for an exam. You do not wait until the night before to check all your notes. You review a little bit each week. Maybe five minutes or ten. That small, consistent attention is what makes the difference. Your budget works the same way.

A weekly review is your chance to see the truth about your money. Where did it actually go? Did you stick to your plan? What worked and what didn’t? These questions sound simple, but most people don’t ask them until it’s too late. By checking weekly, you can catch small problems before they turn into stress or missed opportunities.

Let’s make it relatable. Imagine you planned ₦5,000 for snacks in a week, but by Thursday, you’ve already spent ₦7,000. Without checking in, you might not even notice until the end of the month and suddenly, you feel like your budget has failed. But if you review on the weekend, you see the difference early. You can decide: maybe reduce your snack spending next week, or adjust another category slightly. That little moment of review keeps things from getting out of hand.

Weekly reviews let you celebrate little wins. Maybe you managed to save a bit more than planned, or didn’t overspend on transport. These small victories might feel minor, but when you see them written down, they build confidence.

Even five minutes is enough. You don’t need a complicated spreadsheet or an app. A notebook, a phone note, or even a simple tally works. Small, consistent check-ins like this quietly make budgeting effortless and turn it from a boring task into a real game-changer for your finances.

The important part is consistency. Over time, these small weekly reviews give you awareness, show patterns in your spending, and help you make better decisions before the month ends.

Remember, a budget works when it fits your life. Skip these steps, and you might end up broke, wondering how all your money vanished and trust me, you do not want your next “financial plan” to be sleeping on the street wondering where your snacks went.

In a world filled with endless inspiration, having too many ideas can be just as paralyzing as having none. This article explores how to filter through the noise, identify profitable opportunities, and transform creativity into success.

Planning a trip with friends but worried about your finances? Discover practical budget travel tips, smart saving strategies, and stress-free ways to enjoy group adventures without going into debt. Travel smarter without sacrificing fun.

Learn how to save for your dream vacation without falling into credit card debt. Discover practical budgeting tips, smart saving strategies, and proven financial hacks for stress-free, debt-free travel.