Think budgeting means giving up everything you love? Discover the biggest budgeting myth and how a simple financial plan can actually give you more freedom.

The Budgeting Myth: Unmasking the Biggest Misconception That Holds Your Finances Hostage

Pull up a chair. Pour yourself a cup of coffee and yes, I mean the expensive, frothy, $6 kind from the local café. I promise I am not going to yell at you for buying it.

We need to have a real talk about budgeting.

Let’s play a quick word association game. When I say the word "budget," what is the very first visceral reaction that hits your body?

If you’re like almost everyone I talk to, your chest just tightened a little bit. You probably let out a heavy sigh. Your brain immediately conjured up an image of a tight fist, a stern voice, and the crushing weight of deprivation. You pictured complex, color-coded spreadsheets filled with red numbers. You thought of saying "no" to your friends when they ask you to go out for drinks. You thought of cheap, generic-brand groceries, canceled vacations, and a general, suffocating sense of guilt.

For most of us, the word "budget" triggers the exact same psychological panic as the word "diet."

It feels like a punishment. It feels like a financial straitjacket designed by boring accountants to restrict, control, and frankly, suck all the joy out of your one wild and precious life in the name of being a "responsible adult."

Listen to me carefully: This is the single biggest misconception about budgeting.

The deeply ingrained belief that budgeting is about restriction and deprivation, rather than freedom and empowerment, is a toxic myth. And it is the exact reason why you, and millions of other incredibly smart people, start a budget on January 1st and completely abandon it by January 14th.

We have been culturally brainwashed by old-school financial gurus to believe that embracing a budget means giving up everything we love. We think we have to suffer today so that we can hopefully, maybe, eventually be rich when we are 65 years old and too tired to enjoy it.

What if I told you that this couldn't be further from the truth? What if the very tool you have been avoiding because you thought it would lock you in a cage is actually the only key that can let you out?

Today, we are going to completely dismantle this "budgeting boogeyman." We are going to explore the behavioral psychology behind why we hate the word, expose the real power of a well-crafted financial plan, and redefine what it means to manage your money.

By the end of this conversation, you will never look at a budget the same way again.

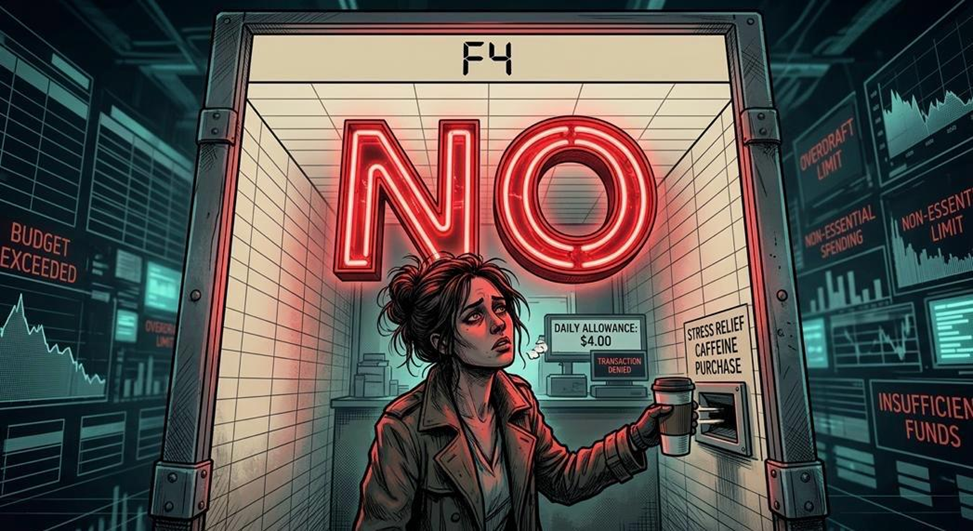

Misconception #1: Budgeting is About Telling You "No"

The idea that a budget is a list of things you cannot have is deeply ingrained in our cultural psyche. It feels like a strict parent standing over your shoulder, slapping your wrist every time you reach for your debit card.

You want to buy that new gadget? No, the budget says no. You want to go out for a fancy dinner to celebrate a promotion? No, the budget says no. A spontaneous weekend trip to the mountains? Absolutely not, the budget won't allow it!

This perspective is fundamentally flawed because it relies on a psychological concept called "ego depletion." This is the proven theory that human willpower is a finite resource, just like the battery on your iPhone.

Think about the diet industry. Imagine you decide to lose weight, so you go on a strict crash diet. You declare that starting Monday, you will eat nothing but boiled chicken breast, steamed broccoli, and water. No sugar. No carbs. No joy.

For the first three days, you rely purely on willpower. You feel disciplined. But by Thursday afternoon, your willpower battery is completely dead. You had a stressful meeting, you're tired, and you walk past a bakery. You smell a fresh chocolate chip cookie, and your brain short-circuits. You don't just buy one cookie; you buy a dozen. You eat them all in your car. And then the shame spiral kicks in: "Well, I already ruined my diet for the week. I might as well order a pizza for dinner and start over next Monday."

If your entire financial strategy relies on you constantly telling yourself “No," you are mathematically guaranteed to fail. You cannot fight human nature forever. Eventually, you will be tired, stressed, or emotional, your willpower will snap, and you will binge-spend.

The Reality: Budgeting is About Telling You "Yes" – to What Matters Most.

A truly effective budget isn't a censor; it is a compass. Better yet, it is a permission slip.

Instead of blindly swiping your card and then wondering where all your money went at the end of the month, a budget allows you to consciously allocate your funds to the things that bring you genuine joy.

Personal finance expert Ramit Sethi calls this finding your "Money Dials." The concept is brilliant and simple: you ruthlessly cut costs on the things you do not care about so that you can spend extravagantly on the things you love. Let's look at a real-world example. Meet my friend Sarah. Sarah loves traveling, and she loves high-quality, specialty coffee. However, Sarah couldn't care less about driving a fancy car or wearing designer clothes.

If Sarah operates without a budget, she lives in a financial fog. She might accidentally lease a ₦837,600 per month (roughly) car because "that's what people do," and she might buy clothes she doesn't need because of targeted Instagram ads. By the time she wants to book a flight to Italy or buy her daily ₦5000 latte, her bank account is empty. She feels broke, restricted, and guilty.

But if Sarah builds a value-based budget, she flips the script. She buys a reliable, used Honda Civic for cash. She buys basic, affordable clothing. Because she intentionally said "no" to the things she doesn't care about, her budget now enthusiastically says "YES" to her true desires. She has a dedicated fund that grows every month, and she has a "Guilt-Free Coffee" category that allows her to buy her daily latte without a single ounce of shame.

• Want to save for a down payment on a house? Your budget helps you say "yes" to that dream by showing you exactly where to cut back on the subscriptions you don't even use.

• Dreaming of a lavish vacation? Your budget helps you say "yes" to that experience by creating a dedicated, automated savings category.

• Love your daily gourmet coffee? Your budget can help you say "yes" to that small pleasure by showing you where you can comfortably fit it in without derailing your retirement.

It's not about stopping you from spending. It's about making sure your spending habits are an exact reflection of your life's priorities.

Misconception #2: Budgets Are Only for People Who Are "Bad With Money"

There is a massive, unspoken stigma attached to budgeting. Many people avoid it because they associate it with financial struggle, poverty, or a lack of self-control.

I hear this all the time: "I make six figures, I'm not broke, so I don't need a budget." Or "Budgeting is for people who are drowning in credit card debt and can't control themselves at the mall."

This elitist view completely misses the point of what a budget actually is. A budget is simply a plan for your capital. Do you think Apple, Amazon, or Google operate without a budget? Of course not. They track every penny, project their revenues, and allocate their capital to maximize growth. If multi-trillion-dollar corporations need a budget to succeed, why would you try to operate without one?

The Reality: Budgets Are for Everyone Who Wants Financial Clarity and Control.

From millionaires managing vast investment portfolios to recent college graduates navigating their very first paychecks, successful financial management almost always involves some form of cash-flow planning. In fact, the more money you make, the more critical a budget becomes due to a dangerous, silent killer known as "Lifestyle Creep."

Lifestyle creep (or the Hedonic Treadmill) is the psychological tendency for your expenses to rise in exact proportion to your income.

When you make $50,000 a year, you rent a modest apartment and drive an old car. You think, "If I just made $100,000, I'd be rich!" But then you get the raise to $100,000. Suddenly, you need a luxury apartment, a leased BMW, and organic groceries. When you hit $200,000, you need a country club membership, private schools for the kids, and first-class flights.

I know people making $250,000 a year who are absolutely terrified of a $500 unexpected car repair. Why? Because without a budget, high earners often find themselves living paycheck to paycheck, just at a much higher, more stressful tax bracket. They have massive cash flow, but zero actual wealth. They are wearing golden handcuffs.

A budget acts as a protective fortress around your future wealth, shielding your hard-earned income from the relentless bombardment of lifestyle inflation.

High earners use budgets to ensure they're maximizing their investments, legally minimizing their tax burdens, saving aggressively for early retirement, and allocating funds to luxury experiences without accidentally overextending themselves. Average earners benefit immensely from budgeting to cover necessities, aggressively pay down student loans or consumer debt, build bulletproof emergency savings, and plan for future goals.

Anyone at any stage can use a budget to gain the ultimate superpower I call clarity. Where is your money really going? Are your spending habits serving your long-term happiness?

A budget provides the raw, unbiased data you need to make informed decisions. It is not a sign of weakness or financial incompetence; it is the ultimate sign of intelligence, maturity, and proactive financial stewardship.

Misconception #3: Once You Set a Budget, It's Set in Stone Forever

The thought of creating a perfect budget on a Sunday afternoon and then having to adhere to it rigidly, without a single mistake, for the rest of your natural life is enough to make anyone throw in the towel.

This perfectionist mindset is why so many budgets fail. People sit down, create a hyper-strict spreadsheet, and vow to never overspend again. Then, three weeks later, life happens. Their dog eats a sock and needs a $400 vet visit. Or they get invited to a last-minute birthday dinner for their best friend. They overspend their "Dining Out" category by $50.

Immediately, the "Screw It" effect kicks in. "I failed. I broke the rules. I'm terrible at this. The month is ruined, so I might as well buy those shoes I wanted." They abandon the budget entirely and go back to blindly swiping their debit card.

The Reality: Budgets Are Dynamic, Flexible, and Evolve with Your Life.

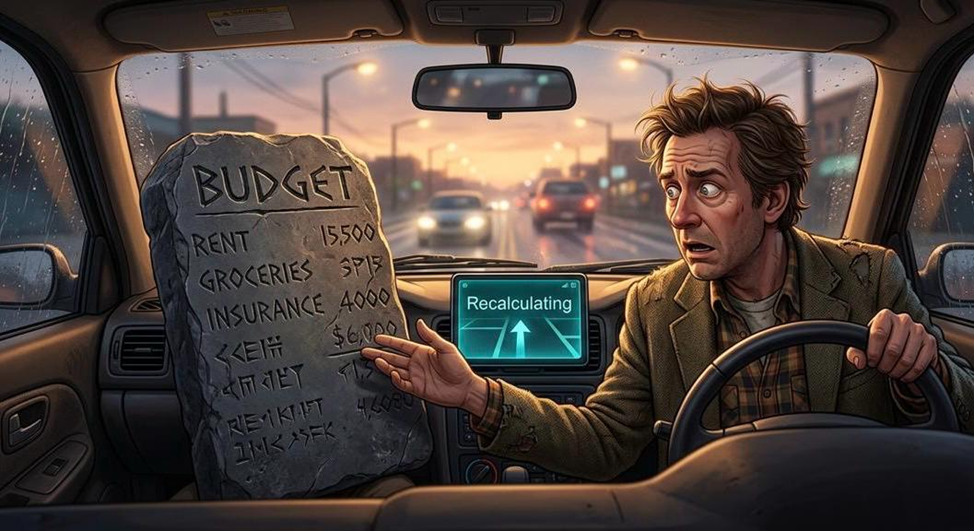

Life is not a static, predictable spreadsheet. Life is chaotic, messy, and constantly changing. Therefore, your budget cannot be a rigid contract written in blood; it must be a living, breathing document.

Think of your budget less like a prison warden and more like the GPS navigation system in your car. When you get in your car and type in a destination, the GPS draws a blue line on the map. That is your plan. But what happens if you miss a turn? What happens if there is a sudden traffic jam, or a road closure, or you decide to pull off the highway to grab a snack?

Does the GPS yell at you? Does it call you a failure? Does it tell you to turn the car around, go back to your driveway, and give up on the trip entirely?

No. It simply says: "Recalculating."

It looks at exactly where you are in that specific moment, and it draws a new line to get you to your destination. That is exactly how you must treat your budget. When something big in your life changes like getting a raise, starting a new job, having a baby, moving to a new city, or even adopting a dog, it usually affects your finances too. Moments like these are a good time to sit down and recalculate your budget.

Your spending naturally shifts throughout the year. Summer might bring vacations, weddings, and more outings, while winter often comes with higher heating bills, holiday gifts, and hosting family or friends. A good budget plans for these seasonal changes.

Hear me, your first budget will be terrible. You will inevitably overestimate how much you spend on gas and wildly underestimate how much you spend on takeout. That is completely okay. Budgeting is a skill, and like any skill, it takes practice. Each month provides new data to refine your allocations and make your budget more realistic for the next month.

When you overspend in a category, you don't quit. You just move money from one category to cover the shortfall in another. You recalculate, and you keep driving.

Misconception #4: Budgeting Means Living a Miserable, Scarcity-Driven Life

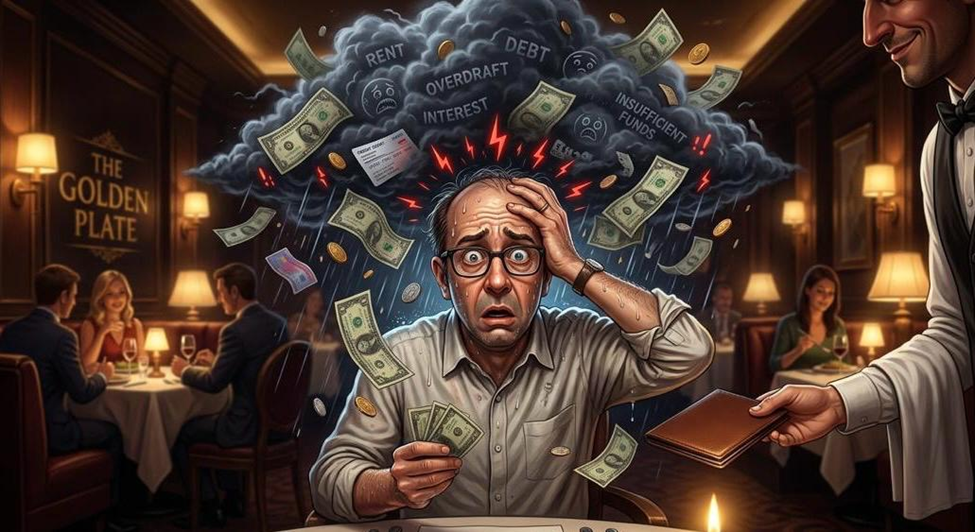

This is perhaps the cruelest and most backward misconception of them all. People fear that budgeting will force them into a life of constant deprivation, where they are forced to count pennies, deny themselves simple pleasures, and live in a state of perpetual scarcity.

But if you look closely at how people without budgets live, you will realize that they are the ones actually living in scarcity.

Uncontrolled, un-budgeted spending is the true source of financial misery. It leads to the low-level, constant hum of anxiety that plays in the background of your life. It is the dread of checking your bank account app on a Monday morning. It is the knot in your stomach when the waiter brings the check, and you pray your card doesn't decline. It is the guilt you feel after an impulsive Amazon purchase. It is the suffocating weight of credit card debt, and the constant, terrifying feeling of never having "enough."

Living without a plan is the true scarcity-driven existence. You are a passenger in your own life, hoping you don't crash.

The Reality: Budgeting Creates Abundance by Eliminating Financial Stress.

A budget, paradoxically, is the greatest tool for creating a feeling of absolute abundance. When you give every dollar a job, you remove the anxiety of the unknown.

When you know exactly where your money is going when your rent is covered, the lights stay on, and you’re setting something aside for the future, it brings a deep sense of calm. That kind of financial clarity helps you relax and quite literally sleep better at night.

Watching your savings slowly but surely grow for that dream vacation, a wedding, or a down payment on a house provides a powerful sense of progress and abundance. You aren't just surviving; you are actively building your dreams.

By planning your spending, you drastically reduce your reliance on credit cards to cover everyday emergencies. Freeing yourself from 24% interest rates and the accompanying stress is the closest thing to magic in the financial world.

Budgeting doesn't force scarcity; it liberates you from it. Think of a playground next to a busy highway. If there is no fence, the children huddle in the center, terrified to play. If you build a strong, secure fence, like a boundary, the children will run freely and joyfully all over the yard. Your budget is the fence that allows you to play freely with your money.

Misconception #5: Budgeting is Too Complicated, Math-Heavy, and Time-Consuming

When many people think of budgeting, they picture a stressed-out accountant hunched over a desk at midnight, surrounded by receipts, punching numbers into a calculator, and managing a spreadsheet with 400 different rows and complex formulas.

If you hate math (and trust me, I am not a math person either), this image is terrifying. The belief that budgeting requires hours of tedious administrative work every single week keeps millions of people from ever starting.

The Reality: Budgeting Can Be as Simple or as Detailed as You Need it to Be.

We live in the golden age of financial technology. You do not need to be good at math to budget. You do not need to save physical receipts. While some people genuinely thrive on granular, detailed financial tracking (and more power to them!), budgeting does not have to be a part-time job.

There are numerous budgeting methodologies, ranging from ultra-simple to highly detailed. The secret is finding the one that matches your specific personality and lifestyle. It's like finding the right workout routine. If you hate running, don't force yourself to run. Find what fits.

In a world filled with endless inspiration, having too many ideas can be just as paralyzing as having none. This article explores how to filter through the noise, identify profitable opportunities, and transform creativity into success.

Planning a trip with friends but worried about your finances? Discover practical budget travel tips, smart saving strategies, and stress-free ways to enjoy group adventures without going into debt. Travel smarter without sacrificing fun.

Learn how to save for your dream vacation without falling into credit card debt. Discover practical budgeting tips, smart saving strategies, and proven financial hacks for stress-free, debt-free travel.