Struggling to pay off debt? Discover why debt is 80% psychology and only 20% math, and learn powerful mindset shifts that can help you finally break free and take control of your finances.

The Psychology of Debt: Why Paying Off Debt is 80% Mindset and Only 20% Math

If debt were just a math problem, absolutely none of us would have it. We would all look at a credit card statement, logically deduce that paying 24.99% annual interest on a pair of shoes or a weekend trip to Vegas is a terrible return on investment, and we’d never borrow a single dime.

But spoiler alert: You are not a spreadsheet. You are a beautifully complex human being with a brain that is biologically hardwired to seek immediate pleasure and avoid immediate pain.

The brutal truth is that the financial gurus in tailored suits rarely admit is that most of the time, especially when it comes to money issues, personal finance is 20% head knowledge and 80% behaviour. Getting out of debt isn't about mastering a calculator or finding the perfect Excel template; it’s about mastering your own psychology. It is understanding why you do the things you do when you are tired, sad, or trying to impress people you don't even like.

Let’s break down the mental game of debt, explore exactly why our brains actively sabotage our bank accounts, and learn how you can hack your own psychology to finally get your balances down to zero.

The Invisible Money Illusion

To understand how to get out of debt, we first have to understand how we accidentally stumbled into it. And let's clear the air right now: it’s usually not because you’re inherently bad with money or because you lack moral character.

Most consumer debt doesn't happen because you woke up one morning and decided to buy a $100,000 speedboat on a whim. It happens through a slow, quiet leak. Think about how your grandparents bought things. If they wanted a new TV or a nice dinner out, they had to drive to the bank, withdraw physical paper bills, drive to the store, and physically hand over a massive stack of cash. That process hurt. Psychologists call this the pain of paying. Your brain registers the physical loss of resources, and it makes you pause and ask, "Do I really need this?"

Today? Money isn't really like that anymore.

Tech companies and banks have spent billions of dollars to remove every single ounce of friction from the buying process. You don't even have to pull out a credit card anymore. You just double-click the side of your phone, the screen scans your face, a little green checkmark appears, and boom, a package shows up on your porch two days later.

When you remove the friction, you remove the pain. Combine this frictionless spending with something psychologists call "Optimism Bias." We are biologically wired to assume that our future will be better, easier, and wealthier than our present. For instance, when you tap your phone to buy those $150 concert tickets, your brain whispers, "It's fine, I'll just pay it off next month when I get my bonus, “or "I'll start budgeting on Monday, so this doesn't count."

We constantly borrow from "Future Us" because we assume "Future Us" is going to be a millionaire with perfect habits and zero stress. But here is the harsh reality: "Future Us" is just "Present Us" living with the decisions we made yesterday.

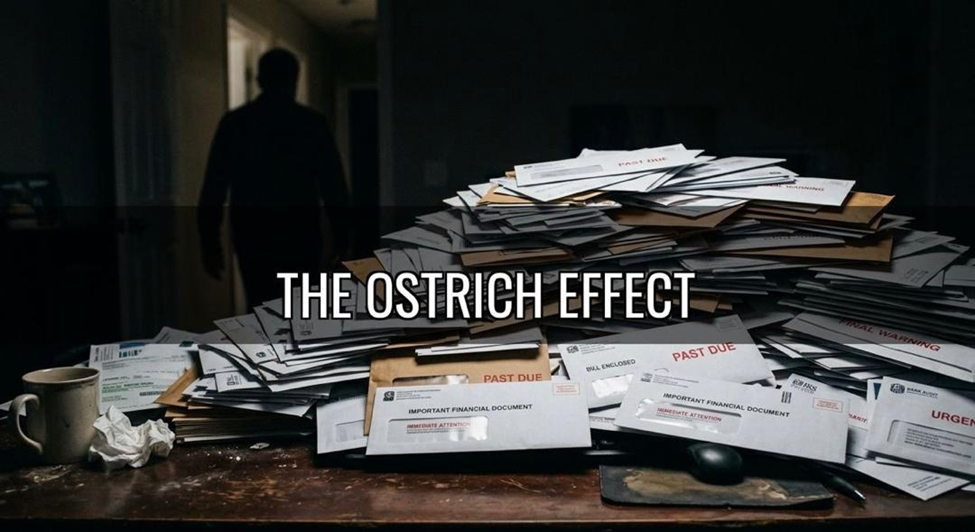

The Ostrich Effect: Why We Ignore the Envelopes

Once the debt starts piling up, a new, incredibly powerful psychological phenomenon kicks in: The Ostrich Effect.

Have you ever received a bill in the mail, looked at the logo on the envelope, felt a sudden wave of nausea, and just shoved it in a junk drawer? Have you ever actively avoided logging into your banking app for three weeks because you were terrified of what the number would be? Have you ever swiped your debit card at the grocery store and held your breath, just praying it goes through?

If I don't look at it, it doesn't exist.

This isn't you being lazy, and it isn't you being stupid. This is your brain’s natural, evolutionary defence mechanism against shame and anxiety.

Debt carries an enormous amount of societal guilt. When we look at our balances, we don't just see numbers on a screen. We see our past mistakes staring back at us. We see the vacation we couldn't actually afford, the college major we didn't end up using, the wedding we overspent on, or the emergency we weren't prepared for. Sometimes just opening the statement is enough to make your chest tighten, your breathing goes shallow, and your stress levels spike.

So, like an ostrich burying its head in the sand, we look away to protect ourselves from the pain. But ignoring the monster in the closet only gives it time to grow. While you are looking away, compound interest is working against you 24 hours a day, 7 days a week. The Ostrich Effect turns a $2,000 problem into a $10,000 disaster.

The "Keeping Up with The Joneses" Illusion

We cannot talk about the psychology of debt without talking about the environment we live in. We are the first generation in human history that watch the highlight reels of 8 billion other people in real-time, 24/7, right in the palm of our hands.

In the 1980s, "Keeping up with the Joneses" meant looking at your next-door neighbour's new lawnmower and feeling a little jealous. Today, it means opening Instagram and seeing a 22-year-old influencer vacationing in a private villa in Santorini, driving a G-Wagon, and wearing a Rolex.

Our brains are tribal. We are wired to want to fit in with the pack, because thousands of years ago, being left out of the pack meant you starved to death. When we see our peers (or people we perceive as our peers) living luxurious lifestyles, our brains signal that we are falling behind. We all feel that little nudge to spend so we can look like we’ve got life together. But here’s the twist: a lot of the people you’re comparing yourself to are just good at hiding their debt.

I always say this. Wealth is what you don't see. When you see someone driving a $90,000 car, the only thing you actually know about their finances is that they have $90,000 less in the bank than they did yesterday (or, more likely, they have a $1,200 monthly car payment that keeps them awake at night).

You are going into debt to impress people who are also in debt. It is a circular firing squad of financial anxiety. Once you realize the game is rigged, you give yourself permission to stop playing.

How to Hack Your Brain to Win the Mental Game

So, if math isn't the answer, if willpower eventually runs out, and if our brains are actively working against us, how do you win?

You need to stop fighting your psychology and start using it to your advantage. You have to trick your brain into wanting to pay off the debt. Here are five psychological hacks to completely change the game.

Hack 1: Forgive "Past You" (The Sunk Cost Fallacy)

You cannot shame yourself into wealth. Let me repeat that: You cannot shame yourself into wealth.

Beating yourself up over the credit card balance you racked up three years ago is burning the exact emotional energy you need to fix the problem today. Guilt says, "I made a bad decision." Shame says, "I am a bad person." Shame will keep you paralyzed.

You have to practice radical financial forgiveness. Take a deep breath and say it out loud: "I made the best decisions I could with the information, the maturity, and the emotional state I had at the time. It’s done. The money is gone."

This is overcoming the Sunk Cost Fallacy. You cannot get the money back that you spent on that stupid timeshare or that overpriced car. Stop mourning the past. Forgive "Past You" for racking up the bill, so "Present You" can get to work building a life for "Future You."

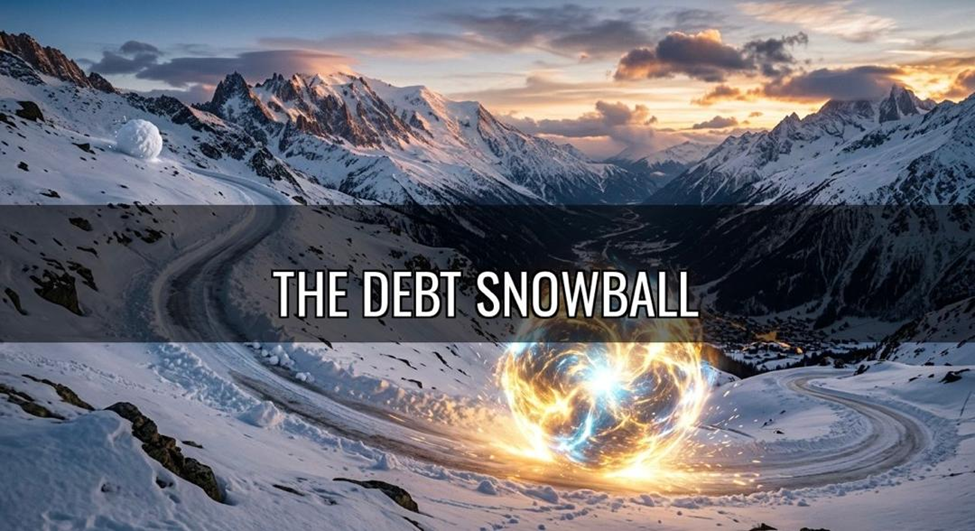

Hack 2: Use the Debt Snowball (Dopamine > Math)

If you ask a math professor or a finance bro how to pay off debt, they will tell you to use the Avalanche Method that involves paying off the loan with the highest interest rate first. Mathematically, this saves you the most money.

But remember, we are playing a psychological game, not a math game.

Imagine you have a $25,000 student loan at 8% interest, and a $500 medical bill at 0% interest. The math says attack the $25,000 loan. But if you do that, it might take you two full years of aggressive payments before that balance hits zero. That is two years without a victory. You will die of Debt Fatigue before you ever reach the finish line.

Instead, use the Debt Snowball. List your debts from the smallest balance to the largest balance, completely ignoring the interest rates. Pay the minimum on everything and attack the smallest one with a vengeance.

Why? Because when you pay off that tiny $500 medical bill in just one month, you get to cross it off the list forever. That psychological height gives you the momentum, the energy, and the belief in yourself to attack the next smallest loan.

Hack 3: Make the Invisible, Visible (Gamify Your Progress)

Debt is invisible. You can't touch it, you can't hold it, and you can't see it sitting in your living room. Because it is abstract, it is very hard for our primitive brains to process our progress. You need to make your progress physical and gamify it.

Think about why video games are so addictive. They give you clear progress bars, levels to unlock, and immediate visual feedback when you do something right. You need to apply this to your debt.

Print out a giant thermometer, a colouring chart, or a paper chain representing your total debt. Tape it to your refrigerator, your bedroom door, or your bathroom mirror. Every time you pay off $100 or $500, take a giant red marker and colour in a line. Or rip a link off the paper chain.

It sounds childish, but I promise you, it works. Humans are highly visual creatures. Seeing that red line climb higher and higher, or watching the paper chain get shorter and shorter, triggers a deep sense of pride and accomplishment that a digital number on a banking app simply cannot replicate. It turns a chore into a game.

Hack 4: Budget for Joy (The Anti-Diet Approach)

If you put yourself on a financial diet of zero fun, zero restaurants, and zero entertainment, you will eventually binge. It is the exact same psychology as a crash diet. To survive the long haul of debt payoff, you must budget for joy.

Give yourself a small, guilt-free allowance every single month. Maybe it’s $40 to buy fancy coffee, $50 to buy a new video game, or $60 for a nice dinner with your partner. The rule is that you can spend this specific money on whatever stupid, fun, frivolous thing you want, completely guilt-free.

By giving your brain a controlled, planned release valve for spending, you prevent the massive, budget-destroying blowouts. A planned $5 coffee keeps you sane; an unplanned $500 Target blackout ruins your month. Budget for the coffee.

Hack 5: Change Your Identity

The stories we tell ourselves about ourselves become our reality. If you constantly walk around saying, "I'm just bad with money," or "I'll always be broke," your brain will subconsciously make decisions to prove you right. It becomes a self-fulfilling prophecy.

You need to change your internal monologue. You are not bad with money. You are simply someone who wasn't taught how to manage money, and now you are learning.

Shift your identity. Start telling yourself, "I am someone who is taking control of my financial future.""I am someone who pays off their debts.""I am a wealth builder."

When you face a temptation to buy something you don't need, ask yourself: "What would a wealth builder do in this situation?" By shifting your identity, you change your behaviour from the inside out, you stop acting like a victim of your circumstances and start acting like the CEO of your life.

The Debt is 80% psychology. It is a mental marathon, not a math sprint. Once you stop fighting the numbers, forgive your past mistakes, and start managing your mind, the math will take care of itself.

You have the power to change your family's entire financial trajectory. You’ve got this. Now go print out a chart, grab a red marker, and get to work.

In a world filled with endless inspiration, having too many ideas can be just as paralyzing as having none. This article explores how to filter through the noise, identify profitable opportunities, and transform creativity into success.

Planning a trip with friends but worried about your finances? Discover practical budget travel tips, smart saving strategies, and stress-free ways to enjoy group adventures without going into debt. Travel smarter without sacrificing fun.

Learn how to save for your dream vacation without falling into credit card debt. Discover practical budgeting tips, smart saving strategies, and proven financial hacks for stress-free, debt-free travel.